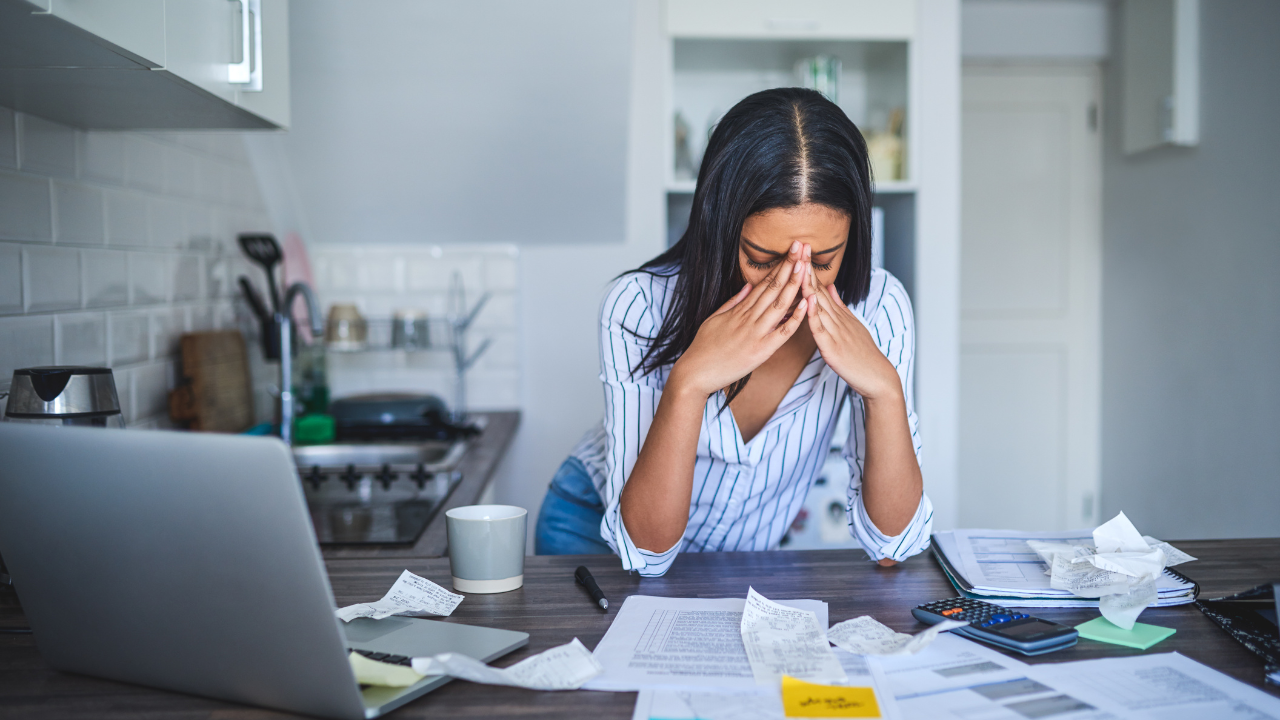

We all have experienced that moment where we realize we messed up with our finances. Your face goes numb. A flush of warmth runs through your body. You want to run…hide…maybe curl into a little ball, never to be heard from again.

Ok, so that’s a little dramatic, but I can tell you from experience that money mistakes can make us behave (or want to behave) in some pretty strange ways.

We all mess up with money. Even the most savvy budgeter (yes, even financial educators like me) can get blindsided by an unexpected expense, get caught up in a moment and overspend, or miscalculate our numbers.

So what can we do when we make a mistake with our money? Here are six tips to help you recover from financial setbacks:

Step 1: Acknowledge the error. The only way to recover from a money mistake is to admit you made one. It might be hard to accept (particularly if the consequences of your mistake are hard), but you can’t fix the problem until you acknowledge it.

Step 2: Forgive. It’s vital to forgive yourself (and potentially others) for the choices that led to this mistake. Maybe you didn’t open a late payment notice in the mail until it was too late, and now owe more than you would have otherwise. Or perhaps you didn’t realize your 401k contributions were sitting in cash for years, instead of growing through investments. Regardless of what the problem was, find a way to release the guilt and shame so you can move forward productively.

Step 3: Assess. Like discovering a mysterious wet spot on the floor, it’s important to assess the damage once you’ve found the problem. Be careful not to catastrophize. Instead, gain clarity around what steps you need to take to get back on track.

Step 4: Get curious. When we make a mistake, it can be easy to want to move on and not think about what happened. But as the old saying goes, “Do not look where you fell, but where you slipped.” It’s important to get curious about what led up to your money mistake. Without judgement or blame, ask yourself:

- What was I feeling and thinking when this happened?

- Who was I with?

- Where did this take place?

- What knowledge or information was I lacking that contributed to this mistake?

Step 4: Recalibrate. This will likely mean getting extremely clear on the real numbers of your financial situation. What would it look like to be out of this hole? Then work backwards on baby steps from there. If this mistake happened recently, you may be able to reverse the damage. Paying a small restocking or cancellation fee might be a far easier pill to swallow than eating the full price of your mistake.

You might need to:

- Cut back on your spending for a while.

- Find ways to increase your income (even for a short period).

- Automate your savings, investments, or bill payments.

- Block out time to call creditors or research your options.

- Creating a written plan and tracking your progress.

Step 5: Be tenacious. If your money mistakes will take many months or years to correct, remember that the time will pass either way. Time matters, and taking action sooner, rather than later, can mean major differences in late payment fees, accrued interest, and legal action (if applicable). It might be scary or embarrassing, but don’t let your feelings get in the way of communicating. Honest and open communication is key to getting back on track. Avoid dwelling on “what-ifs” and “if-only” thoughts – these will only bring you down.

Step 6: Prevent disaster moving forward. If your money mistakes are related to forgetting due dates or late fees, there are so many ways to set up alerts and overdraft protections. This is also an opportunity to garner the motivation to finally get an emergency fund started, or automate wherever possible. Stick to what is actionable and doable.

Remember, you’re a human being and no matter how dire your financial situation may seem, you can regain control of the situation. Do what you can, with what you have, where you are. Every step forward, no matter how seemly small, will get you closer to where you want to be.